Financing Montana Business

Big Sky Finance is a statewide certified development company licensed by the SBA to administer the SBA 504 Loan program in Montana. The SBA 504 Loan program is designed to provide long-term, below-market, fixed asset financing to small, for-profit businesses. The SBA 504 Loan program represents permanent financing and is an economic development program utilizing job creation.

We are here to partner with commercial lenders to provide the best long-term financing tool available to Small Business owners for their real estate and/or equipment financing needs. Leave the SBA paperwork to us – working together, we will make the process simple for you, so you are able to stay focused on serving your customers!

504 Loan Calculator

Enter your project cost and loan rates to determine your estimated monthly payments.

Current Rates

For SBA 504 Loans

Download Forms

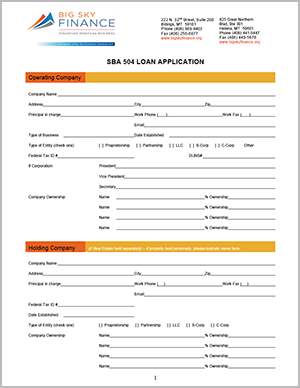

504 Application

504 Application Forms

Borrower Checklist

About 504 Loan Flyer

Let us partner with you on financing

About the SBA 504 Loan Program

Big Sky Finance is here to partner with our lenders in order to provide the best long-term financing tool available to Small Business owners for their real estate and/or equipment financing needs. Leave the SBA paperwork to us – working together, we will make the process simple for you, so you are able to stay focused on serving your customers!

Big Sky Finance is a statewide certified development company licensed by the SBA to administer the SBA 504 Loan program in Montana. The SBA 504 Loan program is a direct SBA lending program designed to provide long-term, below-market, fixed asset financing to small, for-profit businesses. The SBA 504 Loan program represents permanent financing and is an economic development program utilizing job creation.

Eligible Uses

- Purchase land and improvements (operating company must occupy 60% of new buildings and 51% of existing buildings.)

- Construction of new facilities, or modernizing, renovating, or converting existing facilities.

- Refinancing of existing debt in some circumstances.

- Machinery and equipment with a minimum useful life of 10 years.

- Soft costs including but not limited to, title searches, appraisals, environment reports, architect fees, interim loan interest, certain bank fees, furniture and fixtures.

Ineligible Uses

- Inventory

- Working capital

- Intangibles

Small Business Defined As

Tangible Net worth of not more than $15 million and 2-Year average Net Income after taxes less than $5 million.

Economic Development Requirements

- Job creation or retention (one job per every $90,000 borrowed from SBA 504), OR

- Public policy or community development goals met (various options available).

- Manufacturing firm (one job per every $140,000 borrowed from SBA 504)

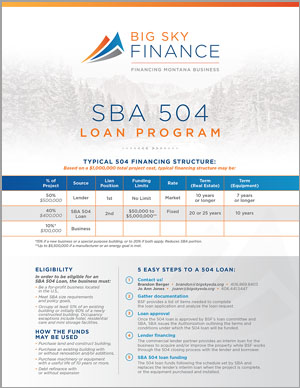

Rates and Terms

- SBA rate fixed for the term of the loan (20- and 25-year rates are tied to the 10-year Treasury bond rate).

- The private lender sets their own rates and fees (commercially reasonable).

- Loan terms are 10, 20, or 25 years (Real Estate: 10-, 20-, or 25-year note, Equipment only: 10-year note).

Fees and Payments

- All SBA 504 loan fees are added to the loan amount and amortized over the loan term. One time processing fee of approx. 2.15% of SBA’s portions, loan closing fees of approx. $2500

- On-going service fee included in the effective full-term rate.

- 10-year prepayment premium on SBA note (20 and 25-year notes)—declining prepayment scale.

Example Of Financing On A Typical $1 Million Project

Total Project Cost:

| Acquisition of Land & Building | $800,000 |

| Improvements | $180,000 |

| Soft costs (appraisal, architect, engineering, closing costs) | $20,000 |

| Total | $1,000,000 |

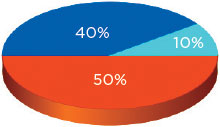

Project Financing:

| Entity | Loan Amount | % of Project | Security |

|---|---|---|---|

| Bank | $500,000 | 50% | 1st Lien |

| CDC/SBA 504 Loan | $400,000 | 40% | 2nd Lien |

| Borrower down payment* | $100,000 | 10%* | |

| Total | $1,000,000 | 100% |

* Start-up OR Special Purpose Building (i.e. car wash, hotel) requires 15% equity. Start-up AND Special Purpose Building requires 20% equity. Borrower down payment can be in the form of: cash, land equity, seller carry-back note (term must match SBA term and be subordinated to SBA if secured by project RE), or any combination thereof.

Typical Deal Structure For An Existing Business Would Be:

- 10% Owner Equity

- 50% Lender Financing (senior position on collateral)

- 40% SBA Financing (junior position on collateral)

Additional equity of 5% or 10% may be required—new business or special property.

504 Process

|

1

|

Contact us!

|

|

2

|

Gather documentationBSF will provide a list of items needed to complete the loan application and analyze the loan request. |

|

3

|

Loan approvalOnce the 504 loan is approved by BSF’s loan committee and SBA, SBA will issue a written agreement that outlines the terms and conditions under which the 504 loan can be funded. |

|

4

|

Lender financingThe lender provides a permanent loan and an interim loan for the business to acquire and/or improve the property while BSF works through the 504 closing process with the lender and business. |

|

5

|

SBA 504 loan fundingThe 504 loan will fund following the schedule set by SBA and will replace the lender’s interim loan when the project is complete or the equipment purchased. |

Testimonials

Kat Healy Red Oxx Manufacturing, Billings

Weston Fricke Simms Fishing Products, Bozeman

Kevin Gustainis, President Montana Peterbilt, Billings

Laura Johnson, Owner The Firehouse Gym, Big Timber

Jeff Johnson, Owner The Firehouse Gym, Big Timber

Funded Projects

Caring Hands Veterinary Hospital

Learn More

406 Window Co. – Billings

Learn More

Cucina Florabella – Missoula

Learn More

Buggy Bath Car Wash – Billings

Learn More

Meadowlark Brewing – Billings

Learn More

J/fit.com, LLC – Whitefish

Learn More

Mint Dental Studio – Bozeman

Learn More

Snyder Motors, Inc. – Bozeman

Learn More

Broadwater Self Storage, Inc. – Billings

Learn More

Backcountry Burger Bar – Bozeman

Learn More

Alpha Omega Disaster Restoration, Inc. – Billings

Learn More

Mountain Hot Tub – Bozeman, MT

Learn More

Daniels Gourmet Meats & Sausages – Bozeman, MT

Learn More

Nelson’s Ace Hardware – Whitefish

Learn More

Restyle Clothing Exchange, Inc. – Missoula, MT

Learn MoreCaring Hands Veterinary Hospital

Caring Hands Veterinary Hospital: A New Chapter in Compassionate Care. The new clinic, a testament to Dr. Herron's commitment to the community and the veterinary field, stands as a symbol of progress and innovation. The newly opened space has been completely remodeled and expanded, offering ample room for more veterinarians, technicians, boarding care staff, and more.

406 Window Co. – Billings

406 Window Co., a retail business operating in Billings since 1995, offers windows and doors for new residential construction projects along with residential remodels. The business has a product for everyone, with product lines ranging from budget to high end, including energy efficient and green options. After many years of building a good reputation and strong client base in the area, owners Brian and Robin Reay were ready to take their business to the next level and set their sights on owning their own commercial building. The nearly 10,000 square foot facility enabled the business to bring all facets of its operations under one roof with an expansive showroom, additional offices, and warehouse space for product storage. Big Sky Finance partnered with Stockman Bank of Billings to provide long-term, fixed rate SBA 504 financing for the construction of the new facility.

Cucina Florabella – Missoula

Cucina Florabella, a contemporary Italian restaurant located on the outskirts of downtown Missoula, was founded by local restauranteurs Ben Burda and Drake Doepke in 2022. With over 20 years of experience in the restaurant industry, Ben and Drake joined forces, venturing into Italian fare for the first time in their careers. Big Sky Finance partnered with First Security Bank in Missoula to provide financing for the purchase and renovation of the property through the SBA 504 program. Seizing the opportunity to fill a gap in the local market for upscale Italian fare, the owners purchased an existing property formerly occupied by a long-time local Italian eatery that closed its doors in the fall of 2021. The duo revamped the restaurant’s concept by extensively renovating the property and creating an all-new menu. The building now features an in-house bakery, a coffee shop, a fully remodeled kitchen, and dining area that provides a uniquely upscale atmosphere the owners call ‘casually gorgeous, friendly yet intimate’. The menu features elevated Italian cuisine with locally sourced products, paired with Italian beer and wines hand selected by sommelier and owner, Ben Burda. Cucina Florabella opened to rave reviews from the local community in December 2022. Big Sky Finance is proud to have worked alongside Ben and Drake to bring their concept to life. The SBA 504 loan program helped make this project possible by affording the owners a lower initial cash contribution along with long-term, fixed rate financing.

Buggy Bath Car Wash – Billings

As a second-generation owner of Buggy Bath Car Wash, Derek Hall was looking to expand the family business and saw a need for a car wash facility on the west end of Billings. Already operating four car wash facilities in Sheridan and Gillette, Billings was a perfect next location, and the corner of Central Avenue and Shiloh Road was the right fit. In the fall of 2022, the Billings Buggy Bath car wash opened offering a state-of-the-art car wash tunnel, an in-bay wash facility, five self-service bays and multiple free vacuum stations - available 24 hours! Big Sky Finance is proud to have partnered with First Federal Bank & Trust on this project for Buggy Bath Car Wash! The total 504 project consisted of the acquisition of the equipment and construction of the Billings facility, debt refinance of the Wyoming locations as well as expansion of one of the Wyoming facilities. This is a great example of the versatility of the SBA 504 Loan program!

Meadowlark Brewing – Billings

Meadowlark Brewing was founded by Travis Peterson and opened its doors in 2014 in Sidney, MT. In 2020, Travis decided to expand the brewery and open a 2nd location in Billings, MT, providing for more capacity and better distribution. Working with Stockman Bank in Sidney, Big Sky Finance provided SBA 504 financing for the construction of the new facility. Construction of the over 20,000 square foot brewery production facility and taproom was recently completed and opened to the public. Meadowlark Brewing is a full production brewery featuring 28 taps and its own canning line. It’s relaxing, family-friendly atmosphere offers a wide array of popular microbrews and excellent bar food. Big Sky Finance is proud to have partnered with Meadowlark Brewing, providing long-term fixed rate financing utilizing the SBA 504 Loan program.

J/fit.com, LLC – Whitefish

J/fit.com, LLC is a woman-owned wholesale distribution company offering their own brand of fitness, sports and outdoor equipment for the at-home exerciser, personal trainer or other sports-minded people. J/fit also supplies their products to retailers nationwide. Loan proceeds were to construct a 13,500 SF warehouse facility, relocating from Vancouver, WA. Financing was provided by First Interstate Bank of Whitefish and SBA 504 loan program as provided by Big Sky Finance.

Mint Dental Studio – Bozeman

In 2011, Dr. Jason Tanguay, DDS purchased the Mint Dental Studio practice utilizing the SBA 504 Loan Program through Big Sky Finance. After continued business growth, Dr. Jason Tanguay, DDS and Dr. Lindsey Hollern, DDS recognized the need for a larger facility. Utilizing the SBA 504 Loan program for a second time, they purchased a new condominium, constructed their tenant improvements, and purchased new equipment. In partnership with First Security Bank, Dr. Jason Tanguay, DDS and Dr. Lindsey Hollern, DDS were able to purchase a new facility to meet their growing needs.

Snyder Motors, Inc. – Bozeman

Owner, Zach Snyder, has been in the used car business for over 12 years with two locations in Bozeman and Belgrade. After renting and outgrowing his location in Belgrade Zach purchased land and constructed a new building about one mile south of his old location utilizing the SBA 504 loan program. In partnership with Opportunity Bank of Montana, this new location provides better customer access and exposure, more parking spaces, and a larger maintenance shop. The ability to obtain affordable financing allows Snyder Motors to grow and focus on their mission of providing a hassle-free car buying experience where the customers needs come first.

Broadwater Self Storage, Inc. – Billings

In order to be eligible for the SBA 504 program a public policy goal must be met, such as being women owned. Broadwater Self Storage, Inc. , is a women-owned 244 unit self-storage facility in Billings. Majority owner, Kendra Daniel and her husband, Roger, took the opportunity to purchase this existing facility which is adjacent to other commercial properties they own. Partnering with Western Security Bank, Division of Glacier Bank (Billings), Big Sky Finance through the SBA 504 loan program provided low down payment, long term, fixed interest rate financing!

Backcountry Burger Bar – Bozeman

In 2017, lifelong restaurateur, Albert McDonald opened Backcountry Burger Bar at a leased location in the heart of downtown Bozeman. An opportunity arose to purchase the historic building he had been leasing for the restaurant. The building is not only occupied by his restaurant but includes an upstairs commercial office space and two residential apartments. Although the SBA 504 Loan Program is for owner occupied properties, it does allow for third party leasing as long as requirements are met. With the SBA 504 loan flexibility and First Montana Bank’s partnership, Albert is now able to own a piece of Bozeman history and continue to serve the community it’s locally sourced and made-from-scratch meals.

Alpha Omega Disaster Restoration, Inc. – Billings

Alpha Omega Disaster Restoration, Inc. is a woman-owned business that has been in the Billings area since 2006 and provides water, fire and mold restoration services. Owner Julie Johnson, along with her husband Willy Johnson consolidated two business locations into a larger facility and utilized the low, fixed long term rates of the SBA 504 loan program to accomplish this goal. Big Sky Finance partnered with Altana Federal Credit Union in Billings in providing financing for this project.

Mountain Hot Tub – Bozeman, MT

Mountain Hot Tub has been owned and operated by Kelly King and his wife Shirley since 2013. Their business has showrooms across Montana in Bozeman, Butte, and Helena. Mountain Hot Tub is one of the top hot tub and sauna dealers in the state. Kelly utilized the SBA 504 loan program through Big Sky Finance, along with lending partner First Security Bank, a Division of Glacier Bank based in Bozeman, MT to construct a new $5 million facility in Bozeman. This move allowed for a larger showroom and warehouse along with consolidating staff and service departments under one roof. As a Navy veteran, King and his wife continue to support the local non-profit Warrior and Quiet Waters for Veterans by donating hot tubs.

Daniels Gourmet Meats & Sausages – Bozeman, MT

Daniels Gourmet Meats & Sausages had the opportunity to purchase the building they had been leasing. Financing was provided by First Montana Bank, Inc. (Bozeman) and the SBA 504 loan program offered through Big Sky Finance. Daniels Gourmet Meats & Sausages is a locally owned and operated artisan meat market featuring local beef, pork, poultry, and lamb.

Nelson’s Ace Hardware – Whitefish

Nelson’s ACE Hardware has been owned by Marilyn and Richard Nelson since 1976 and was located in downtown Whitefish since the 1970's. Due to space constraints which hampered future growth, the Nelson used the SBA 504 loan program through Big Sky Finance, along with lending partner First Interstate Bank in Whitefish to construct a larger facility six blocks away. The project included constructing a brand new 13,300 SF building, 51 paved parking spaces, landscaping, curbs, pole lighting, storm water retention area, and concrete walks around most of the building.

Restyle Clothing Exchange, Inc. – Missoula, MT

Alice Wilmett, owner of Restyle Clothing Exchange, purchased and made some minor repairs to an existing building in a Federal HUBZone which revitalizes the Missoula business district. Financing was provided by First Interstate Bank (Missoula) and the SBA 504 loan program offered through Big Sky Finance. Restyle Clothing Exchange is a woman-owned business that buys and sells gently used clothing for teens and adults.